Last month, we at Polymath Ventures had the opportunity to virtually attend the 3-day Global SME Finance Forum. Sponsored by the IFC, this year’s event was attended by 2400+ individuals from 950+ institutions in 140+ countries. Unsurprisingly the focus this year was on how COVID-19 had impacted SMEs. The pandemic has thrown the world into great uncertainty, turning the way we live and work completely topsy-turvy, perhaps forever in some ways.

Earlier this year, Polymath Ventures and Aflore joined IFC’s SME Finance Forum membership network. The 200+ global members form a close-knit community of industry experts who share a common purpose of helping SMEs. “We believe in the power of the collective and understand the impact of a large network on driving business growth. The association with the Forum will enable us to further provide value to our users, create new opportunities, and design solutions for sustainable economic development,” said Carlos Fernandez de la Pradilla, Founder and CFO of Polymath Ventures.

Certainly, the disruptions and negative effects are too numerous to count—not the least of which include the unfortunate loss of life and the millions of individuals around the world who have been plunged into poverty. But the pandemic has also brought about a massive opportunity, and with it come certain implications for how the ways we do business can and should evolve.

“Given that SMEs account for 60%-70% of GDP, 90% of businesses, and 50% of jobs across countries worldwide”, the focus of this year’s forum was to explore both the challenges and opportunities in SME finance moving forward.

IFC / SME Finance Forum

Highlights

The first day was focused on examining how COVID-19 impacted SME finance across the landscape of players including SMEs, financial institutions, regulators, and fin-techs.

On the second day, we heard from different institutions—including DFIs, banks, credit card companies, fin-techs, and policymakers—on the measures they have taken to respond to the pandemic.

On the final day, a variety of thought leaders shared their predictions for the future of SME Finance, including how both SMEs and the institutions that support them would likely evolve over the next 10 years.

Aside from listening to the keynote speakers, the platform provided opportunities to simulate in-person conferences by offering opportunities for one-on-one networking, virtual marketplaces, exhibition booths, fireside chats, and much more.

How COVID-19 impacted SMEs?

The final impact of COVID remains to be seen as both the health crisis and the financial situation continues to evolve with no immediate end in sight. But the pandemic has already had a profound impact on SMEs both financially and operationally.

The full extent of the pandemic’s effect is still unknown. It is difficult to measure, given the high level of informality in the global SME segment as well as the uneven impacts across geographies and sectors.

Still, some clear trends have emerged giving us broad indicators of how the SME landscape is changing:

- Many SMEs were unable to weather the crisis and were forced to shut down, especially informal firms and those in the hospitality & services sectors; some estimates ranged as high as 20% of all SMEs globally went out of business.

- The lockdowns accelerated the shift to digital: consumers habits have moved toward e-commerce and companies are adjusting to extend periods of remote working.

- Women-led SMEs were generally the worst hit due to women having a heavier burden of domestic duties, unequal access to financing, and overrepresentation in hardest-hit sectors.

How institutions are supporting SMEs (Finance)

Outlook for SMEs in the mid-to-near term is bleak, as recovery is expected to be slow and uneven. This is exacerbated by an ongoing health crisis that is ever-changing, especially now that certain European and US cities are heading into the second round of lockdowns.

Still, there is reason to be hopeful that SMEs will be able to weather the crisis. Multilateral institutions are countercyclical, fin-techs are experiencing unprecedented growth, and governments were quick to recognize solvency issues. All of which have positioned these institutions to better support SMEs through the liquidity crunch.

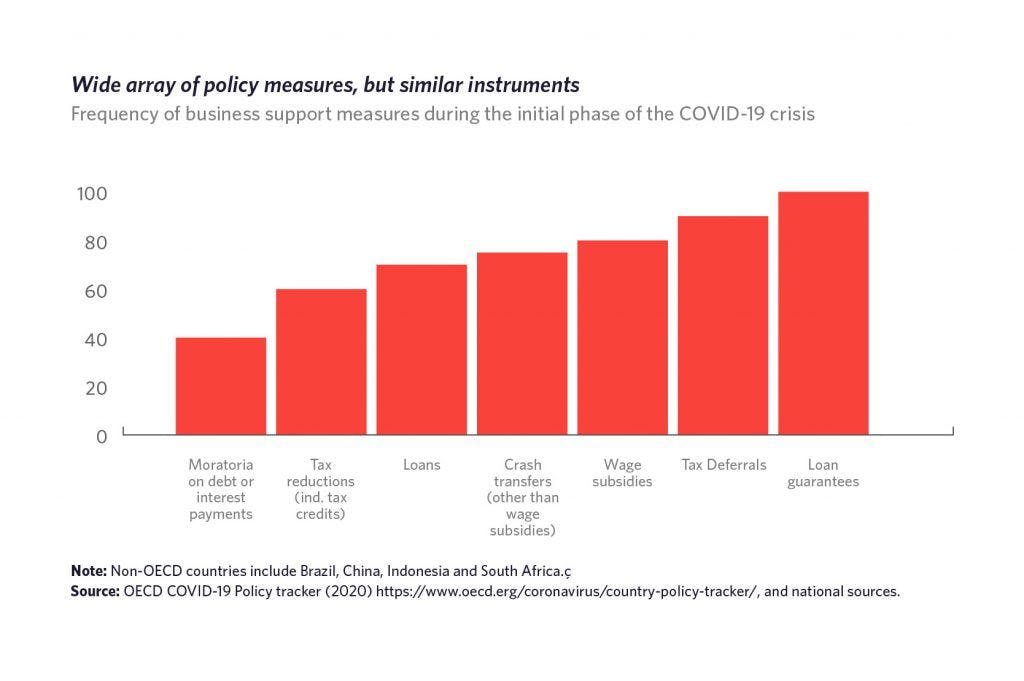

Policymakers worldwide have generally been leveraging the same tools including moratoriums, loan guarantees, and tax deferrals.

Banks and credit card companies have been working to offer more financial products to SMEs, along with expanding access and offering more favorable terms.

DFIs have been injecting more capital to defend their current portfolios and participate in new investments. Fin-techs have been leading the charge in alternative financing and expediting credit decision-making.

Lastly, many institutions have been working to educate SMEs on factoring and reverse factoring financing solutions to help companies stay solvent, during a time when their customers have been slower to pay their invoices on time.

How institutions are supporting SMEs (Non-Finance)

Along with financing, institutions have also been providing Non-Financial Services to SMEs. These holistic suite of services, they feel will give them an edge against competitor institutions and enable greater value creation for their SME customers in the long-term.

Such non-financial services include information exchange, training, consultancy, networking, and partnerships.

In particular, these institutions have been working to train and support SMEs in accelerating their shift to digital, including areas such as: instituting cashless payments, developing a digital brand identity, and optimizing remote working.

Future outlook of SME financing

With the pandemic, several headwinds have emerged that give us some insight into how the SME finance landscape will evolve over the next ten years:

- Rise of fin-techs and alternative financing (e.g. revenue-based financing, crowdsourcing)

- Symbiotic relationship between banks and fin-techs as complementary strategic partners

- Major legal and tax policy changes to reduce the compliance burden on SMEs

- Shifting focus of DFIs toward high-growth SME startups with more flexible financing instruments (equity, Tier 2 capital, lending to NBFIs)

- Use of blockchain, machine learning, and artificial intelligence for instantaneous decisioning with predictive financing (e.g. pre-approvals, credit facilities).

The role of SMEs after COVID-19

Over these three days, getting to learn from thought leaders at the top of their fields was a humbling experience. But more than anything it reaffirmed the importance of the work we do here at Polymath Ventures.

As we continue to watch the pandemic unfold, two things have been made painfully clear over the last few months.

The first is that SMEs are the lifeblood and growth engine of a healthy economy. When we create the optimal conditions for SMEs to flourish and grow, we all stand to benefit. Conversely, when SMEs hurt, we will all feel the consequences.

The second is that the pandemic has in some ways forever altered our behaviors. It has uprooted the way we think, work, and go about life. It has also accelerated some pre-existing trends, especially with e-commerce and digitalization.

Like it or not, the digital revolution is here to stay. To stay competitive, companies must adapt quickly, innovate, and evolve.

We at Polymath are obsessed with creating high-growth digital companies from scratch that solve the needs of underserved populations. In doing so, we hope our ventures will help fill the “missing middle” of SMEs and serve as an engine of growth in the region.

After all these years, it is reaffirming to know that COVID or not we were on the right path all along. At Polymath we aspire to be an agent of change, doing our part to lead the charge and partnering with formidable organizations such as the SME Finance Forum along the way.