We wanted to explore how VCs in Latin America invest in different countries, so we examined 34 of LatAm’s most active VCs that have made 1,524 investments in startups from 25 countries for $20B since 2018. As you can see, the trends are quite different from country to country.

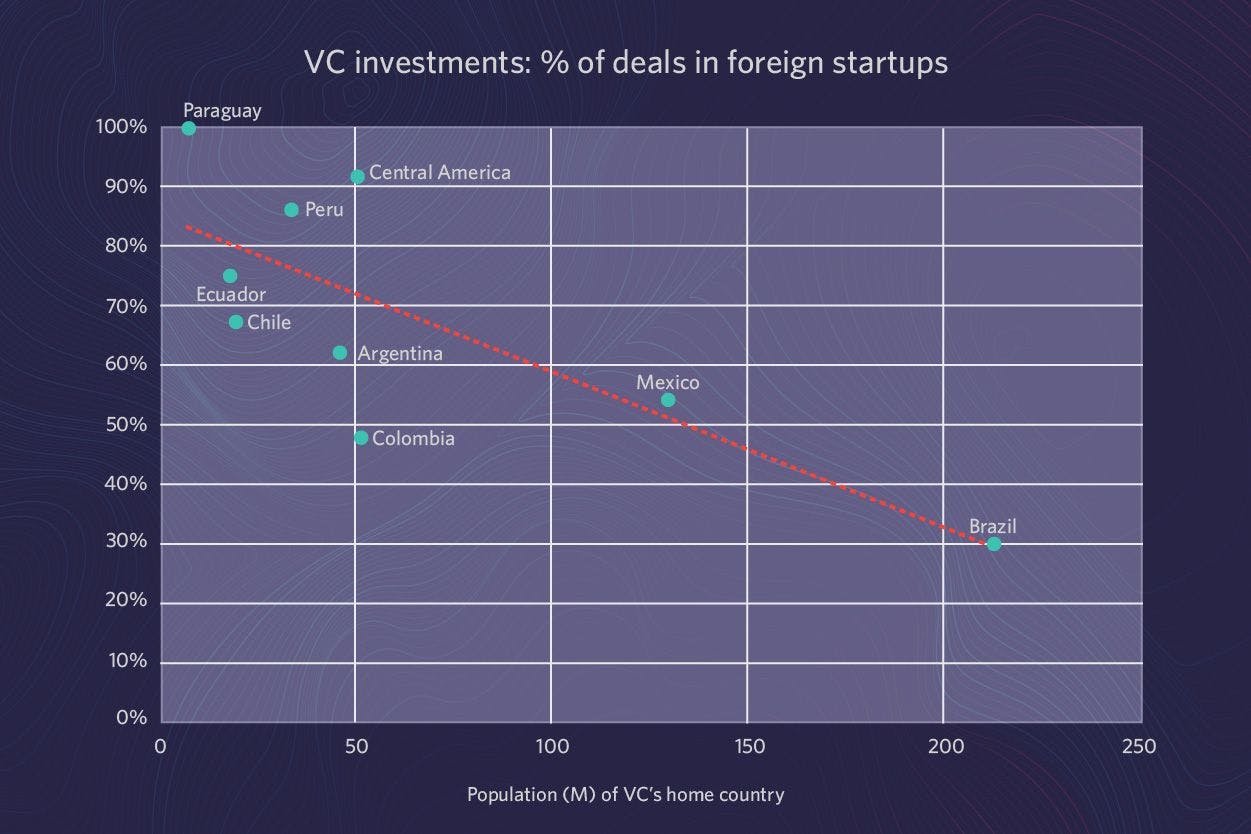

We compared the percentage of investments in foreign startups with the population and GDP of a VC’s home country. Naturally, VCs located in large countries invest more in local startups, while VCs in smaller countries need to look outward to foreign startups for sufficient deal flow, but there are a few interesting outliers.

Peruvian VCs invest more heavily in foreign startups than would be expected from its population and GDP. Peruvian VCs aren’t necessarily neglecting local startups in favor of foreign alternatives (37% of the investments in Peruvian startups were made by local VCs, which is roughly in line with the rest of the region). Rather, this is largely due to the fact that Peru produces relatively few startups. Since 2018, Peru has had 0.7 VC-backed startups per 1M people, which is only ahead of Ecuador (0.5 startups per 1M people) and Central America (0.2 startups per 1M people).

Other indicators such as human capital indices, education attainment, GDP per capita, and inequality can’t explain this phenomenon as Peru is generally on pace with LatAm’s startup leaders Brazil, Mexico, and Colombia.

The concentration of population in Lima should also help facilitate innovation and presents a massive first market for would-be startups. This warrants further investigation into factors such as tax and labor laws, cultural factors that affect the attractiveness of entrepreneurship and working for startups, technical training opportunities, and capital controls. It could also indicate that Peru is due for a startup boom in the near future. In the meantime, Peruvian VCs are finding deal flow by investing heavily in startups from the US and Colombia (Peruvian VCs made 44% of all investments in US startups and 21% in Colombian startups).

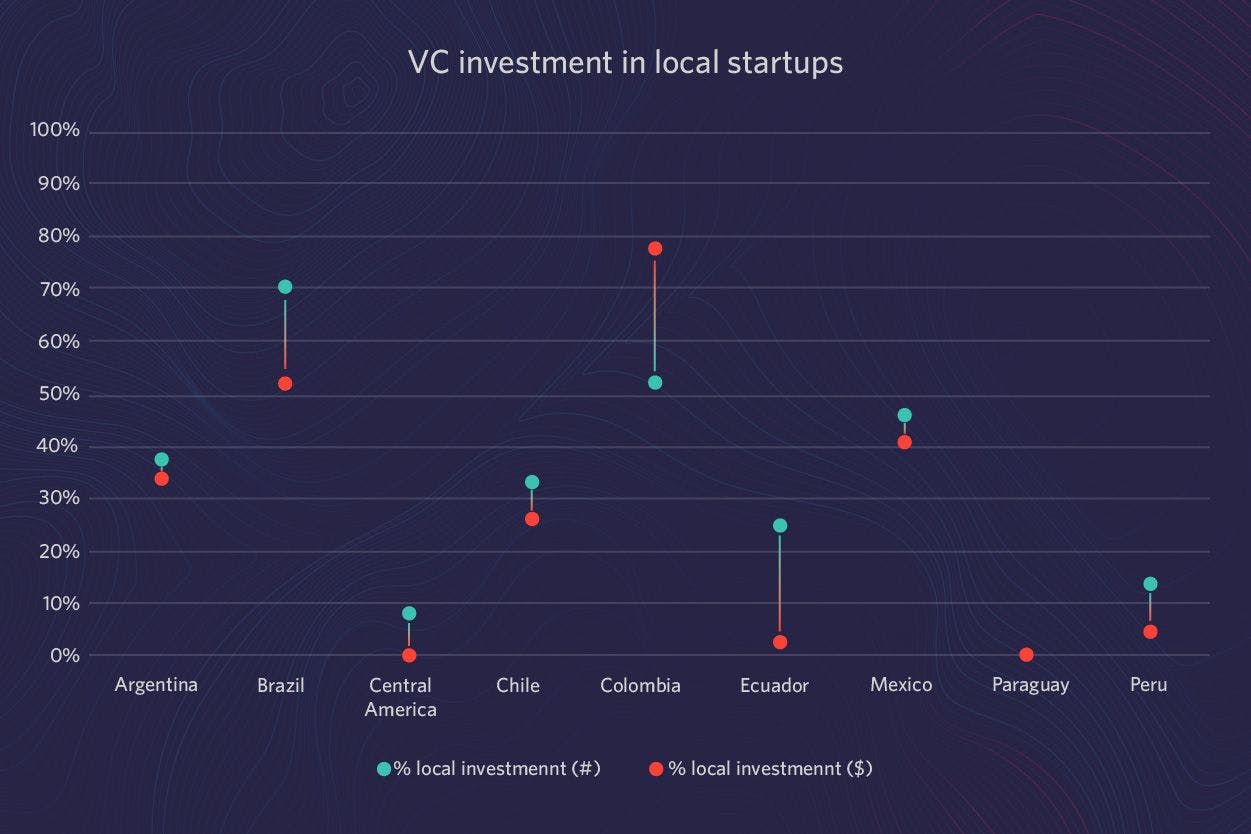

Colombia is an interesting case that suggests there is a significant lack of local investors relative to the amount of Colombian startups.

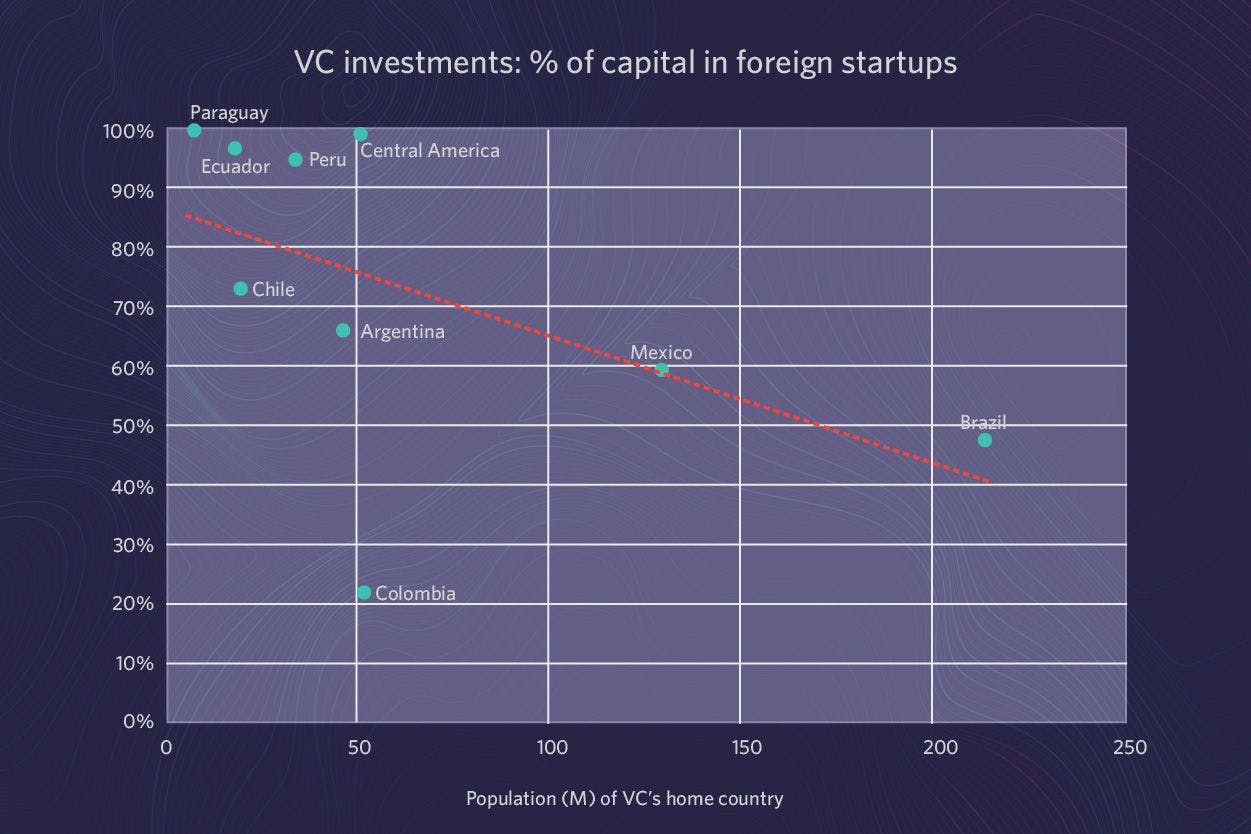

There is a strong trend showing VCs throughout the region invest a higher percentage of capital in startups from other countries compared to the percentage of the number of investments in startups from other countries. In other words, VCs are more likely to do relatively larger deals in foreign startups and relatively smaller deals in local startups.

This makes sense as both sourcing and evaluation of early-stage startups tend to rely on personal networks more than later-stage deals. It’s much easier for a later-stage startup with multiple years of track record to catch the attention of investors, while companies just getting started have to rely much more on warm intros from their own networks. Naturally, these networks tend to be stronger within a startup’s local market.

The only exception is Colombia, where VCs invest a higher percentage of capital in Colombian startups than the percentage of the number of investments they make in local startups.

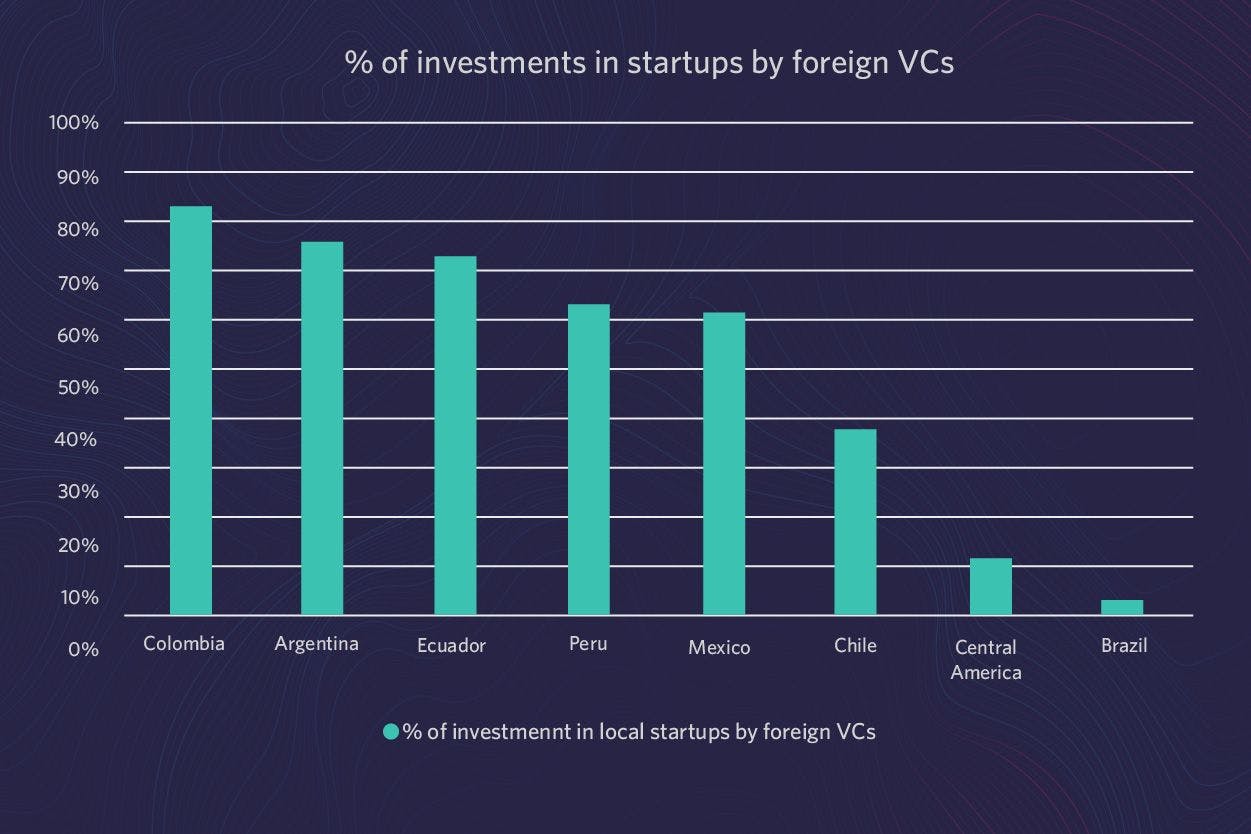

We next examined how many startups from specific countries raised capital from foreign VCs:

Again, Colombia is an outlier with 84% of investments in Colombian startups coming from VCs outside of the country. So while Colombian VCs are heavily focused on local deals (and even more focused on large local deals), there is still plenty of “room” for foreign investors.

The difference is especially stark when compared to Brazil: Brazilian VCs make 73% of their investments in local startups, while only 3% of investments in Brazilian startups come from foreign VCs. This means that Brazilian VCs cover almost all local startups while still making a quarter of their investments in foreign startups. Colombian VCs are similarly focused on local startups, but it’s not near enough to meet local demand, so foreign investors fill the gap.

The dominance of Brazilian VCs of their local market can at least partially be explained by the country's massive size (no need to look outside when there are plenty of local deals to be had) and the more pronounced differences between Brazil and other countries (language, culture, etc.) that make it more difficult for foreign VCs to enter the market.

Colombia’s seeming lack of VCs is more difficult to explain. VC activity usually goes hand-in-hand with startup activity, and Colombia ranks 3rd in LatAm in the number of startups and amount of VC investment, 2nd in VC investment per GDP, and 5th in VC investment per population. Similar to Peru’s seeming lack of startups, Colombia’s seeming lack of VCs warrants further investigation into factors such as tax law, capital controls, a culture of risk aversion, etc. But based on Polymath’s decade of experience, none of these factors offers a satisfactory explanation, and Colombia appears ripe for more investors.

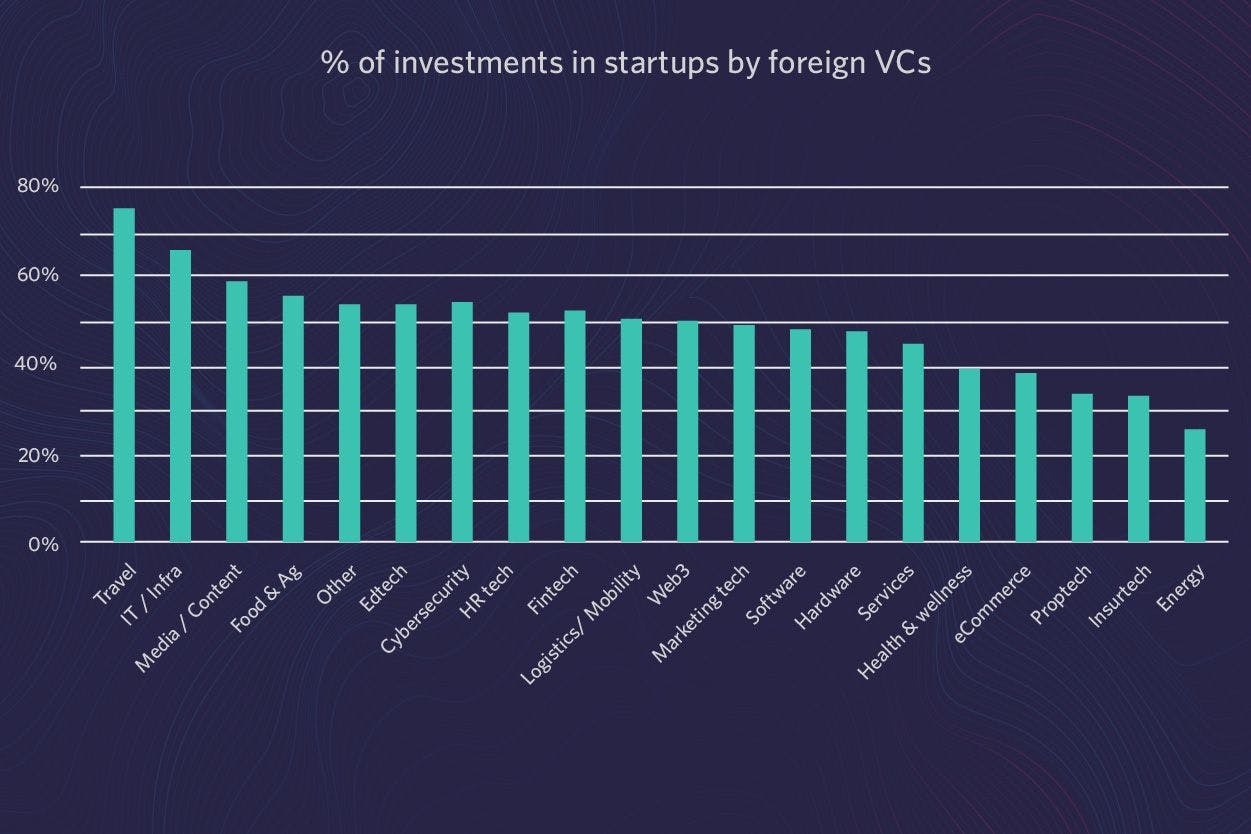

There were also some interesting trends related to how startups from certain sectors are more or less appealing to foreign investors.

VCs are less likely to invest in startups from other countries that operate in heavily regulated sectors such as energy, insurance, healthcare. The lack of foreign investment for sectors such as proptech and eCommerce is less obvious.

Conclusion

Despite the proliferation of VC investment in LatAm over the past several years, the deployment of capital is far from uniform throughout the region. This highlights opportunities for investors to fill gaps in potentially overlooked markets. It also highlights the increased role local VCs can play in attracting foreign capital and getting foreign investors familiar with the nuances and opportunities in their home markets.