Overview

Financial inclusion is one of the most pressing and challenging issues to tackle worldwide. Access to financial services reduces inequality gaps by offering both merchants and individuals products to save income, finance consumption and invest in the future.

Governments and traditional private institutions have implemented policies and introduced products to the market in an attempt to improve financial inclusion – with largely unsuccessful results.

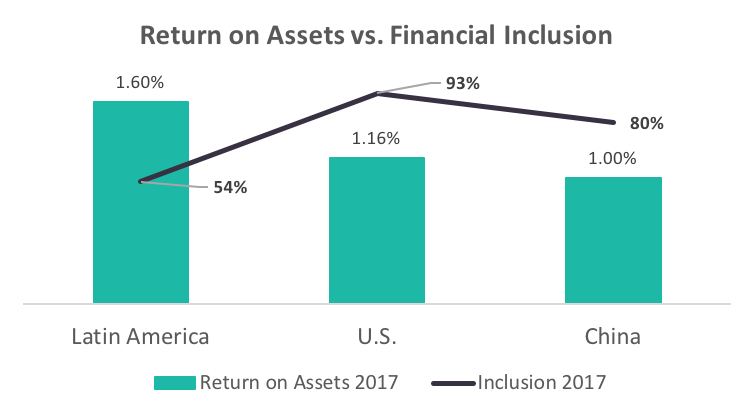

In Latin America, financial inclusion is extremely low for both individuals and small business owners. Only 54% of the adult population has a bank account and 41% have debit cards – In contrast, 94% of adults in high-income countries have an account with a financial institution, with 83% having a debit card.

According to The World Bank, small and medium-sized enterprises (SMEs) in Latin America represent 90% of all firms across the region and employ around 68% of the workforce. However, the financing gap for these enterprises is estimated to be around 250 billion dollars – almost equivalent to Chile’s GDP. This funding gap leaves small merchants with few options to grow and access untapped consumer segments.

Fintech in Latin America is improving financial inclusion by building inclusive, consumer-centric products. Significant technology adoption in the region allows fintech companies to leverage technology and data to reach consumers and businesses.

This article explores the different factors that make fintech the strongest solution to financial inclusion in Latin America. On the one hand, the lack of incentives for traditional institutions to innovate and engage the unbanked has left huge whitespaces to innovate. On the other hand, improved IT infrastructure and a more flexible regulatory framework are enabling new companies to thrive, leveraging a better understanding of consumer behavior to capture underserved needs.

Market dynamics in Latin America

The problem with traditional financial institutions

Commercial banks are the pillar of economic development and financial inclusion in developed countries. They stimulate growth by financing consumption and business expansion and by ensuring consumers against financial shocks.

In Latin America, however, commercial banks have failed to stimulate inclusive growth because their business models, which are copycats of developed market banks, do not understand the middle and lower-class demographics and SME’s, and therefore cannot serve them properly.

Additionally, the oligopolistic nature of these economies leaves the major banks without much competition (and therefore pressure to innovate). This is proven by the statistics which show that Latin America’s most profitable banks are enjoying a much higher return on assets (ROA) compared to bulge bracket banks in the U.S. or China while failing to achieve financial inclusion.

In countries like Brazil, the top five banks supply 95% of the market – showing an oligopolistic market structure and a lack of competition.

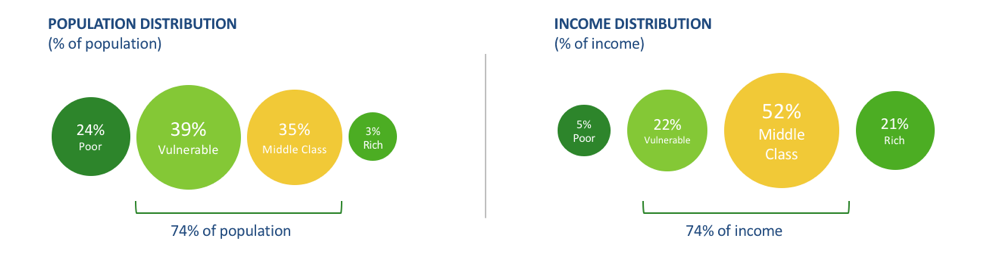

Because of this lack of competition, Latin American banks have dedicated little resources to gather and analyze data to understand their customers better, and have instead focused on products to cover higher income classes. In some instances, they only offer credit cards to users in the top 10% income bracket and disregard the needs of the middle and lower classes, a demographic that makes up 74% of total income and population in Latin America.

SME’s suffer from similar issues. Large banks in the region are handsomely profiting from serving large corporations and have no need to develop financial products and infrastructure that can stimulate small enterprise growth. Specifically, banks have failed to developed transactions products with a price-point accessible to SMEs or the infrastructure to implement payment processors. In addition, banks have failed to develop credit risk models to serve small companies in a sustainable way and often require large volumes of documentation that significantly increase time-to-market.

Consumers and SMEs have turned to the informal market to serve their financial needs.

Consumer behavior in Latin America

In addition to the market gaps caused by banks mentioned above, there is also a significant lack of trust from consumers thanks to the many financial shocks and scandals that have happened in Latin America over the last four decades. From periods of severe debt crisis or high currency volatility to money laundering scandals and stock market scams, the region has seen it all – and financial institutions have failed to restore trust.

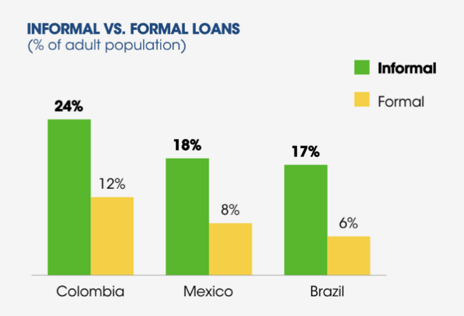

The combination of banks’ shortcomings and a lack of consumer trust have led middle-class consumers and SMEs to prefer the informal market for financial services. Informal loans, for instance, are still commonplace throughout the region – in some cases almost three times as common as formal credit.

In Colombia, people create small savings and lending clubs called “Cadenas”, where the aggregated pool of funds rotates amongst a group of friends. In México, these clubs are called “Tandas”, and about 31% of the adult population participate in them.

This behavior shows that, although there is little engagement with formal financial institutions, the middle class have a deep need, ability and willingness to pay for financial services. The informal market survives on trust and open communication channels in a close, familiar network. It’s a system that consumers understand and can rely on.

The system also gives the population access to a lump sum of money that is otherwise inaccessible and offers an “alternative” savings plan for those who can’t afford banks’ costly administration fees.

In Colombia, 85% of commercial transactions are done in cash due to SME’s low adoption of electronic payments. As a result of not keeping track of commercial transactions electronically, SMEs often have to optimize their inventory manually, keep track of their sales ad-hoc and pay large fees to access credit from informal lenders who don’t require collateral proof.

The problem with these informal markets is that they do not provide long-term solutions. In lending, for example, they provide short-term emergency loans but are unable to give access to the long-term, larger loans that help people build assets.

By understanding how consumers behave in informal markets, fintech businesses can understand the core needs and motivations of the unbanked and develop products to serve those needs.

The enablers

Technology adoption in Latin America

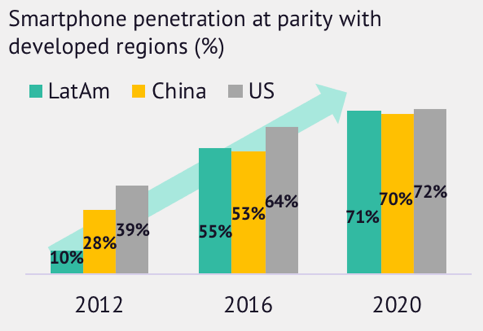

Latin Americans are now more connected. With a smartphone penetration nearing 71% (at parity with China and the U.S.), Latin Americans are more informed and are putting more emphasis on the convenience of hand-held devices to manage their lives.

Fintech companies are leveraging the use of smartphones to access customers efficiently, create a strong user experience and gather better data. Click-through rates, time spent in-app or in-product, adoption of loyalty programs or real-time surveying are some of the metrics that companies are using to add value.

Fintech companies are learning about consumers’ deep financial values. This constant feedback loop is a key differentiator and is positioning these companies as reliable “financial companions”.

Pro-fintech regulatory reform in Brazil, Mexico, and Colombia

Regulators in Brazil, Mexico, and Colombia are pushing fintech growth, implementing a series of open-banking initiatives as the foundation. All three countries have established Fintech Associations that communicate with regulators and have developed structured and controlled environments where fintech companies can test their products in real time.

Main regulatory concepts:

Fintech Sandbox: a framework put in place by a financial industry regulator that allows fintech companies to live test their product in a small-scale, controlled environment supervised by the regulator. The main goal of this framework is to test the viability of innovation while maintaining customer security and control.

This initiative has many advantages. It reduces time-to-market, limits cost, helps regulators and fintech companies identify potential security issues before they become threatening and allows both parties to develop a cooperative environment better suited to support future innovation.

Open-banking policy: a policy that facilitates the exchange of consumer data via shared API’s. This policy allows financial institutions to better keep up with consumer demand data being collected by fintech companies. In turn, fintech companies have access to historical consumer data and can make better decisions when building new business models.

In the end, this is great news for both fintech companies and consumers, who greatly benefit from the new products being continuously launched.

In future articles, we will specifically explore how different regulatory concepts and policies are being implemented in Brazil, Mexico, and Colombia.

The opportunity

Fintech adoption and investment growth

Market dynamics, increasing technology adoption, and regulatory reform create significant white spaces for fintech companies.

Fintech companies are already taking advantage of these white spaces and gaining consumers’ trust. According to the Fintech Adoption Index published by Ernst and Young, Brazil and Mexico have a 40% and 36% average adoption rate for fintech products in 2017, above the 33% world average.

Brazil showed the highest adoption rates for any country in Latin America for Payments, Lending and Enterprise Financial Management, ranking amongst the highest in the world.

International investors are starting to recognize the opportunity in the region. Since 2013, the number of international investors committing capital to Latin American startups has more than doubled. In 2017, 25 of the most renowned international venture capital firms made their debut investments, including Softbank and TPG’s Rise Fund. Some notable fintech investments include Tencent’s $180 million investment in Nubank and Softbank’s $100 million investment in Clip earlier this year.

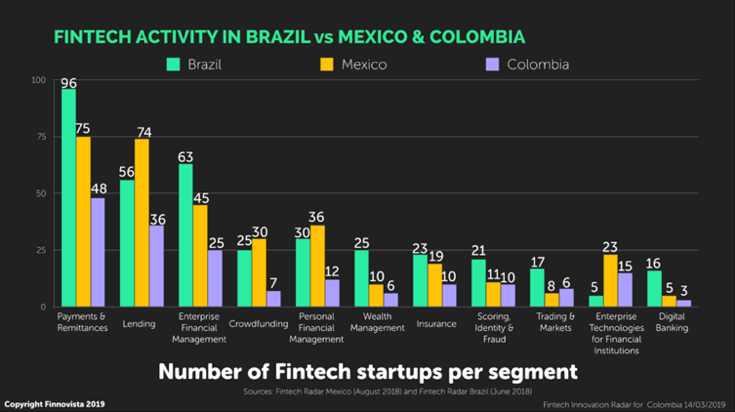

The fintech industry currently hosts 1,166 startups across eleven segments. From a transactional point of view, Payments and Remittances lead the fintech ranks in Latin America, with over $90.5 million worth of transactions across 285 different startups in 2018. Lending services and Enterprise Financial Management take the second and third spots, with 181 and 90 startups seeking to disrupt each segment respectively.

Net Growth in the number of new fintech startups in 2018

Fintech investment in the region grew by 66% to $337 million in 2018. Furthermore, the average investment ticket size bumped up 180% from $3.4 million to $9.6 million between 2017 and 2018 – a sign of increased market maturity.

At the moment, Brazil, Mexico, and Colombia are the most active countries in Latin America, hosting almost 70% of all fintech startups in the region.

A scalable ecosystem

Similar market dynamics across Latin America, low cultural barriers and improving regulation are a recipe for high scalability across the region.

In terms of market dynamics, there are uniform socioeconomic structures and high mobile penetration levels across all countries. Financial inclusion is low across Latin America, with banks lacking the incentives to tackle the underserved and informal markets dominating.

Cultural barriers of communication, mindset, and behaviors between countries are very low. Aside from Brazil, there is a common language. This allows fintech companies to build local products that are relevant to most consumers in the region.

Finally, although regulation is still a barrier, every major country in Latin America has established Fintech Associations that compile information on consumer dynamics, regulatory updates and have open communication channels internationally. This cross-border flow of information allows fintech companies to understand business dynamics and regulatory differences in other countries even before they enter a new market.

This combination of similar market dynamics, low cultural barriers and improving regulation provide fintech companies with a unique opportunity to build highly scalable regional businesses.

—

Stay tuned! In our next article, we will explore the key fintech sub-sectors in more detail and show case studies of how specific startups are disrupting these spaces. Follow us on Medium and LinkedIn to stay up to date.